Research & Evidence · Executive Briefing · AI Transformation

The AI Statistics & Evidence Briefing 2026

AI adoption is mainstream. Transformation is early. The executive evidence base on adoption, financial impact, productivity, workforce change and the workflow redesign gap.

Executive summary

AI adoption has moved from experiment to mainstream business reality. The evidence now shows a clear gap between access, usage and genuine transformation. Most organisations now use AI somewhere in the business, but far fewer have redesigned workflows, changed jobs, embedded agents into daily work or achieved measurable financial impact.

The headline is simple: AI adoption is high. AI transformation is still early. This briefing provides the hard numbers executives need — 12 key statistics, four infographics, and practical conclusions for moving from pilots to measurable business value.

The adoption story is no longer speculative

Stanford’s 2025 AI Index reported that 78% of organisations were using AI in 2024, up from 55% the previous year. McKinsey’s March 2025 survey found that 71% of organisations were regularly using generative AI in at least one business function. By McKinsey’s November 2025 survey, that figure reached 88%.

The adoption story is therefore no longer about whether AI will enter the workplace. It already has. The more important question is whether organisations are changing quickly enough to capture the value.

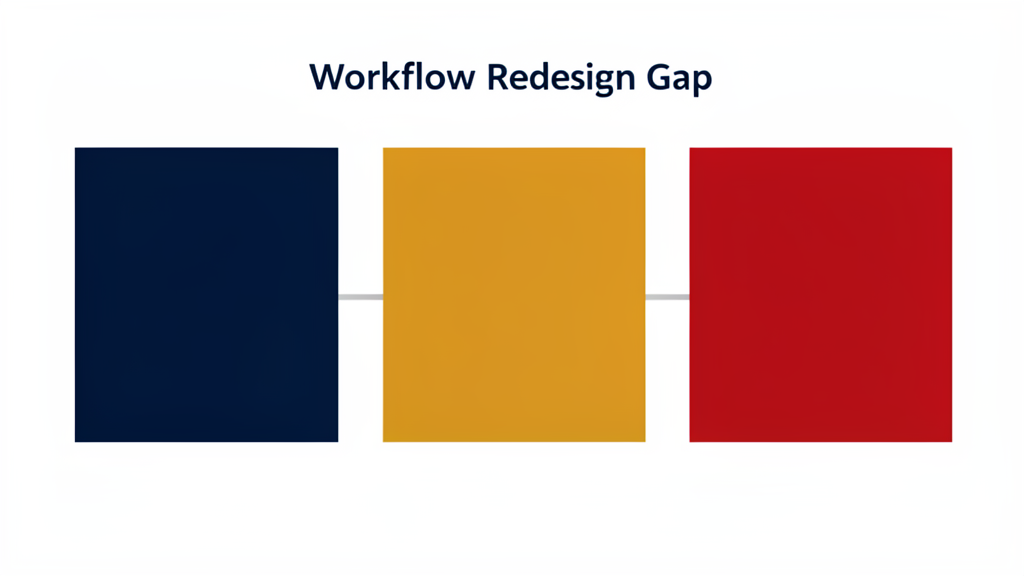

The missing link: workflow redesign

The main barrier is no longer tool availability. It is work redesign.

McKinsey’s March 2025 survey found that workflow redesign had the strongest effect on whether organisations saw EBIT impact from generative AI. Yet only 21% of respondents said their organisations had fundamentally redesigned at least some workflows.

BCG reached a similar conclusion: only 13% of employees saw AI agents deeply integrated into daily workflows. Deloitte’s 2026 State of AI in the Enterprise report adds another hard data point: 84% of companies have not redesigned jobs or the nature of work around AI capabilities, despite high expectations for automation.

Organisations are adopting AI tools faster than they are redesigning work. This is why so many companies report high usage but limited bottom-line impact.

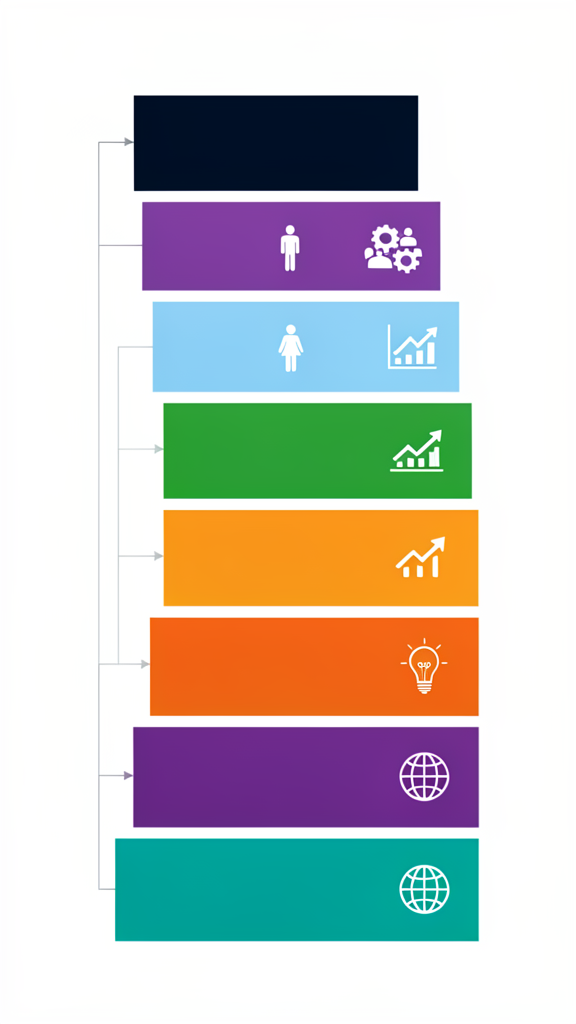

Understanding the AI Value Creation Ladder

One reason AI discussions become confusing is that organisations use the term “AI value” to describe very different outcomes. Saving ten minutes writing an email and fundamentally changing a business model are both examples of AI value, but they sit at opposite ends of the scale.

The AI Value Creation Ladder provides a useful framework for understanding where organisations currently are and where the largest financial benefits emerge.

| Level | Benefit Category | Typical Outcome |

|---|---|---|

| 1 | Individual Productivity | Faster writing, summarisation, coding, analysis and administration |

| 2 | Team Efficiency | Reduced effort, fewer manual tasks, improved throughput and response times |

| 3 | Cost-to-Serve Reduction | Lower operating costs, automation of repetitive work, reduced handling effort |

| 4 | Margin Improvement | Improved EBITDA, higher operating margins, reduced labour cost per unit of output |

| 5 | Revenue Growth | More sales capacity, faster proposals, improved customer experience, higher conversion rates |

| 6 | New Products & Services | AI-enabled offerings, premium services, digital labour, agentic solutions |

| 7 | Business Model Transformation | New markets, platform models, digital workforce integration, industry disruption |

Most organisations currently operate between Levels 1 and 2. Employees are saving time and becoming more productive, but relatively few organisations have redesigned workflows sufficiently to reach Levels 3, 4 and 5, where meaningful financial benefits begin to emerge.

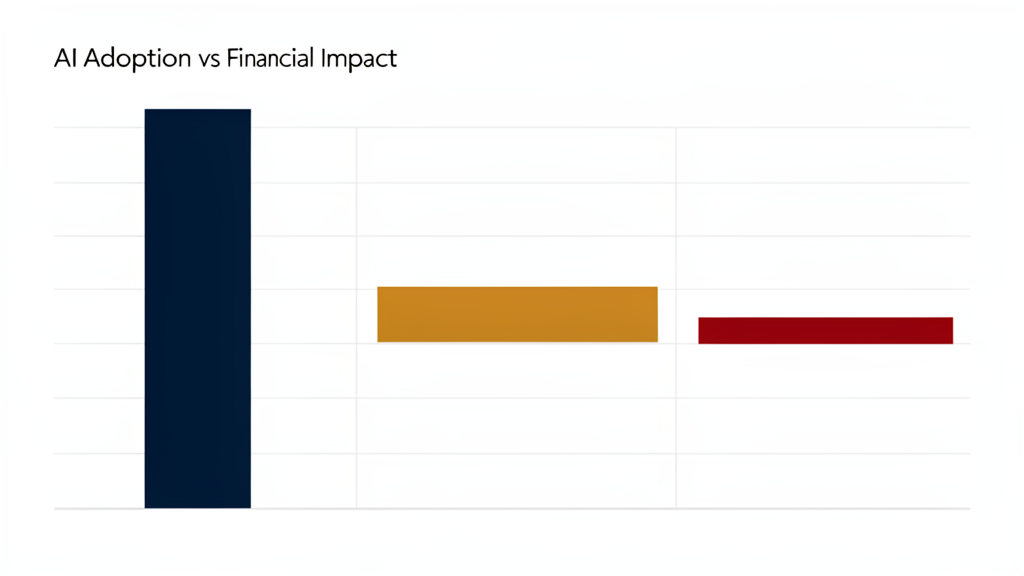

Financial benefits are real but concentrated

McKinsey’s 2025 global survey found that while 88% of organisations use AI in at least one business function, only 39% report measurable enterprise-level EBIT impact. This highlights the gap between adoption and value realisation.

The strongest reported benefits today are productivity, efficiency and cost-to-serve improvements rather than broad revenue transformation. Deloitte’s 2026 research found that 74% of organisations expect AI to contribute to future revenue growth, but only 20% are currently seeing measurable revenue impact.

BCG’s 2026 AI at Work study helps explain why financial value is leaking. Among regular frontline AI users, 42% report saving around eight hours per week — roughly one working day. However, 66% receive limited or no guidance on what to do with the time saved, and more than half are not redirecting that time into higher-value work.

In effect, many organisations are creating capacity but not converting that capacity into EBITDA, margin improvement, revenue growth or lower cost-to-serve.

Productivity gains are real, but uneven

Brynjolfsson, Li and Raymond’s study of more than 5,000 customer-support agents found that generative AI increased productivity by around 14–15% overall, with gains exceeding 30% for less experienced workers. The study also suggests that AI can help spread the practices of stronger workers to less experienced colleagues — effectively making parts of the “team brain” more accessible.

However, Dell’Acqua and colleagues’ “Jagged Technological Frontier” study found that AI improved performance on tasks within its competence boundary but could reduce performance when users applied it to tasks outside that boundary.

AI can be powerful, but not universally reliable. Organisations need training, judgement, governance and clear boundaries.

AI agents: high expectations, early integration

BCG found that 75% of respondents believe AI agents will be vital for future success, yet only 13% say agents are currently integrated broadly into workflows, and only about one-third understand how they function.

Microsoft’s 2025 Work Trend Index describes the emergence of “Frontier Firms” built around human–AI collaboration, digital labour and new “work charts” rather than traditional organisation charts. 45% of leaders say expanding team capacity with digital labour is a top priority over the next 12–18 months.

Shadow AI is both risk and diagnostic signal

Microsoft’s 2024 Work Trend Index found that 78% of AI users were bringing their own AI tools to work, rising to 80% in small and medium-sized companies. This “bring your own AI” trend cuts across generations.

This creates risk: data leakage, intellectual property exposure, compliance problems, privacy concerns, poor-quality outputs and hallucinated answers.

However, shadow AI is also a diagnostic signal. Where shadow AI appears most strongly, official workflows may be too slow, too painful or too poorly supported. The mature response is not simply to ban AI. Organisations generally need to move through four stages: Ban → Tolerate → Govern → Enable.

Key statistics at a glance

| Theme | Statistic | Source |

|---|---|---|

| AI business adoption | 78% of organisations used AI in 2024 | Stanford AI Index 2025 |

| GenAI adoption | 71% regularly used GenAI in at least one function | McKinsey, Mar 2025 |

| AI adoption | 88% used AI in at least one business function | McKinsey, Nov 2025 |

| Enterprise EBIT impact | 39% report measurable enterprise-level EBIT impact | McKinsey, Nov 2025 |

| Workflow redesign | 21% had fundamentally redesigned at least some workflows | McKinsey, Mar 2025 |

| Agent integration | 13% saw AI agents deeply integrated into daily workflows | BCG, 2025 |

| Agent expectation | 75% believe AI agents will be vital for future success | BCG, 2025 |

| Job redesign gap | 84% had not redesigned jobs around AI | Deloitte, 2026 |

| Revenue impact | 20% are currently seeing revenue growth from AI | Deloitte, 2026 |

| Revenue ambition | 74% expect AI to contribute to future revenue growth | Deloitte, 2026 |

| Shadow AI | 78% of AI users brought their own AI tools to work | Microsoft, 2024 |

| Time saved | 42% of regular frontline AI users saved ~8 hours/week | BCG, 2026 |

| Value leakage | 66% receive limited/no guidance on saved time use | BCG, 2026 |

| Productivity gain | 14–15% productivity improvement in customer support | Brynjolfsson et al. |

| Novice productivity gain | 30%+ productivity gain for less experienced workers | Brynjolfsson et al. |

| AI skill wage premium | 56% wage premium for workers with AI skills | PwC, 2025 |

| Worker usage | 50% of employed US adults use AI at least a few times yearly | Gallup, 2026 |

Move from pilots to measurable transformation

The evidence is clear: AI adoption is mainstream. Transformation is early. The organisations that will capture sustained financial value are those that combine technology with workflow redesign, workforce trust, governance, skills development and operating-model change.

Talk to Mission Institute about AI readiness